Reveal

Potential

Reach the heights of trading with us! We offer a wide range of trading accounts suitable for traders of all levels.

Get Started

First steps

How to Start Earning

1step

Think

Consider several ways to earn money on the exchange. Assess their advantages and disadvantages. Choose among them the most suitable for you.

2step

Choose

Find several tools on our platform for investing and choose among them the most suitable one. Register and open a minimum deposit.

3step

Earn and Learn

Try different approaches, learn from your actions, gain experience. Analyze your steps, work on your mistakes, improve your skills and strategies.

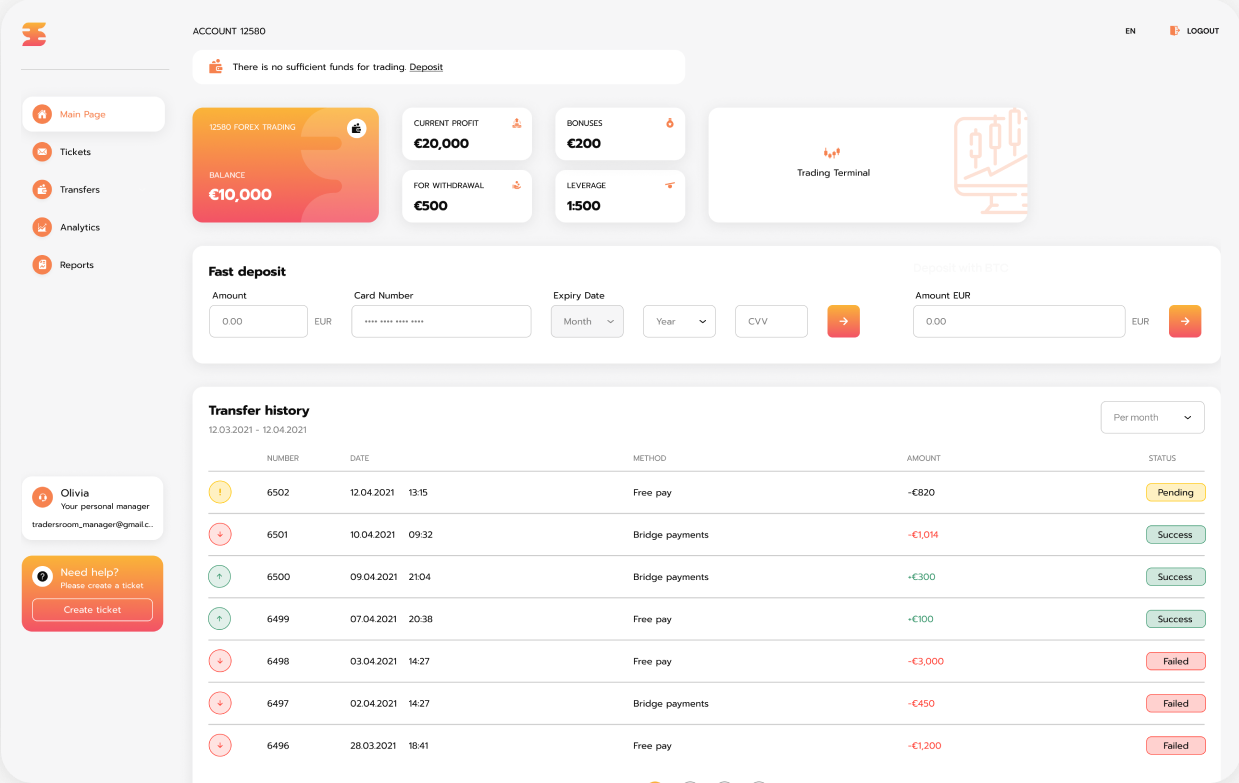

Features

Open a World of New Financial Opportunities

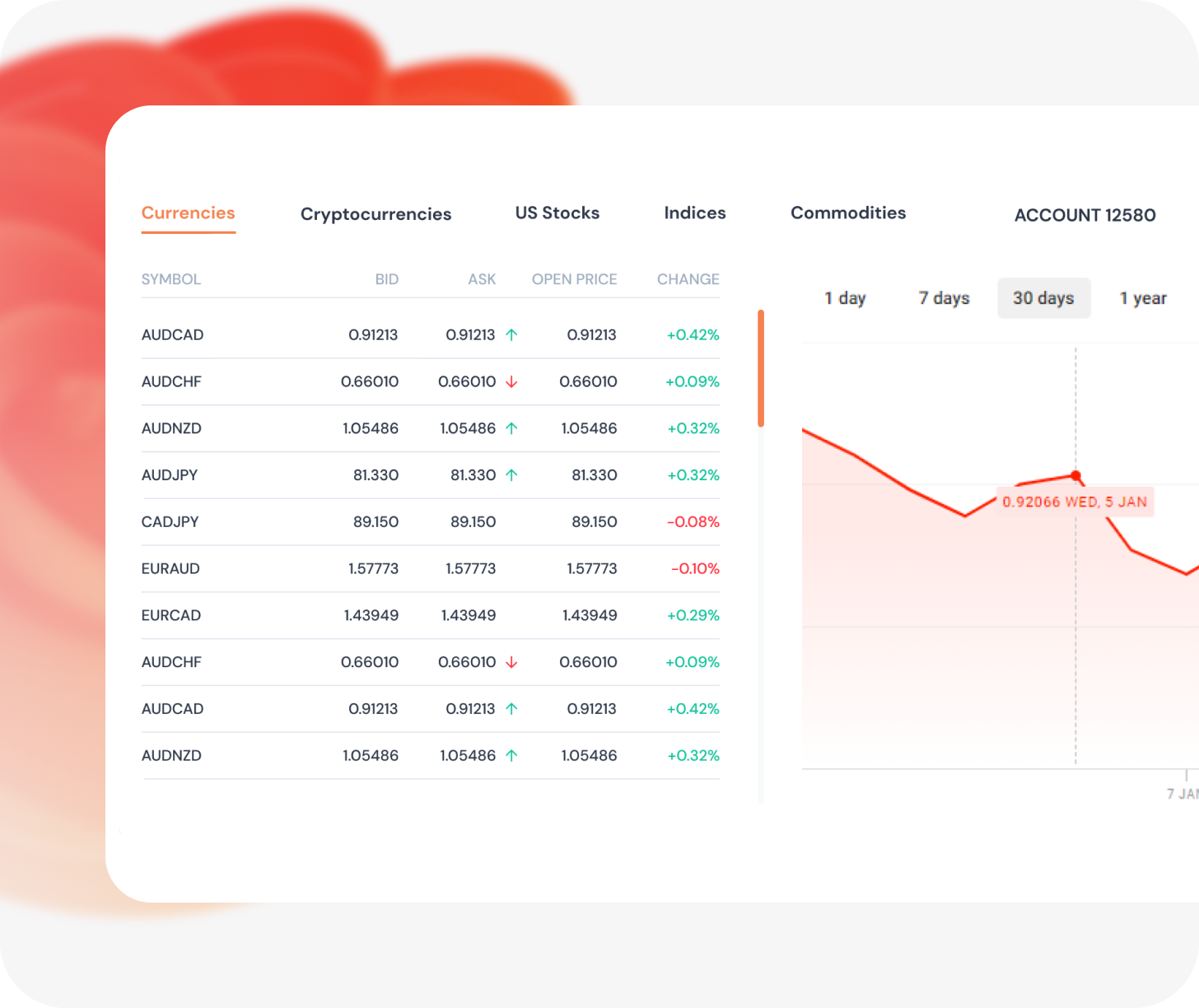

Investments

Explore a wide range of trading instruments, carefully selected for their high liquidity, allowing you to make optimal investment decisions.

Analytics

Gain access to exclusive market research empowering you to learn how to predict chart movements alongside our team of traders.

VIP Club

Join an international community of traders and unlock privileges that are typically unavailable to the majority of market participants.

Safety

The real-time margin calculation system reflects the market revaluation of all client positions, ensuring an accurate risk.

Explore a variety of options and trade with confidence, taking advantage of global market trends and making informed investment decisions.

Custom reports

Personalized Reports Customized for Your Needs

Every trader has unique requirements for analyzing and monitoring their trading activity. That's why our company provides customized reports specifically tailored to each client's needs. Our team of professionals works closely with traders to create personalized reports that highlight performance metrics, market analysis or visualization of specific data.

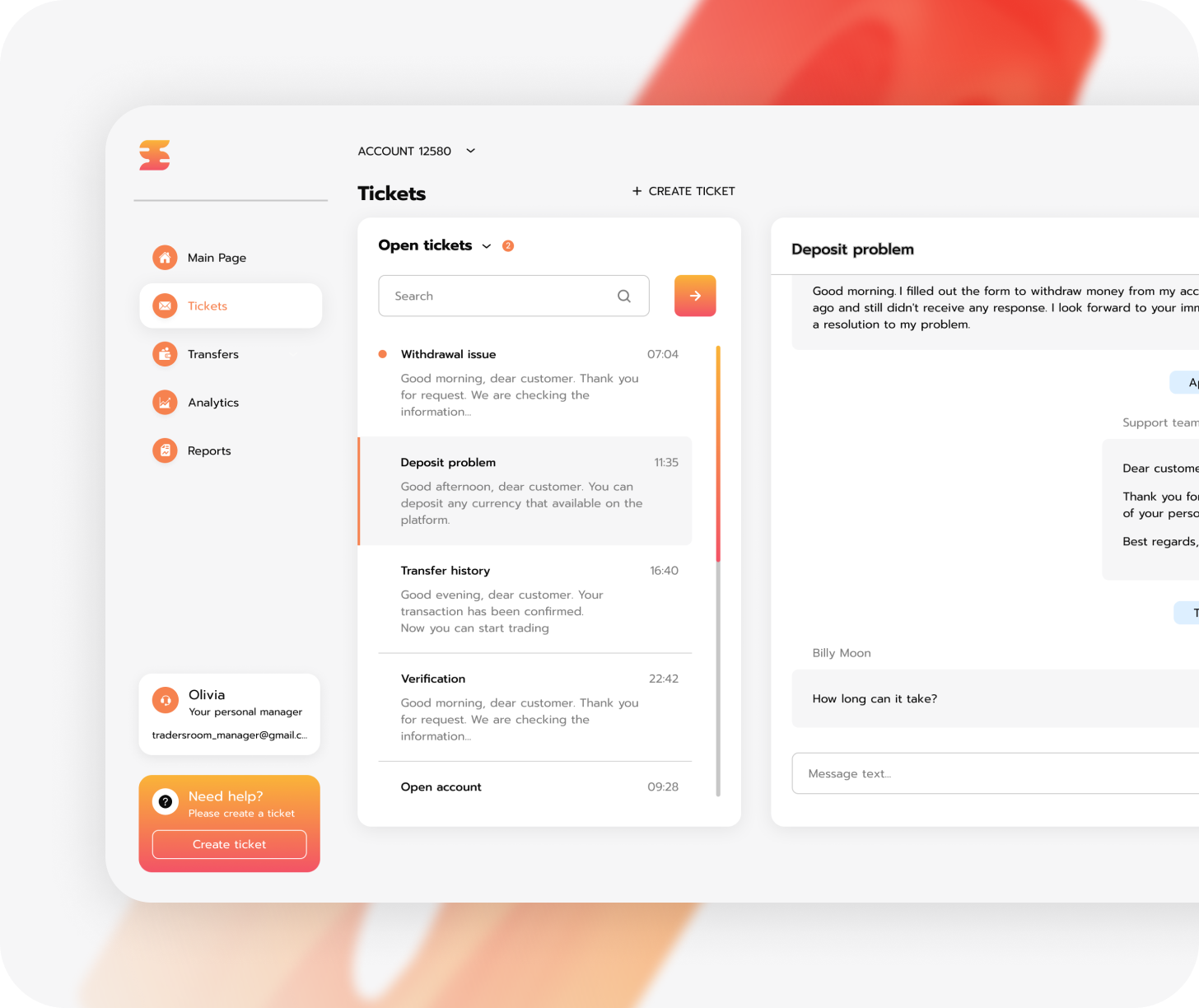

Personalized support

Comprehensive Support Service for Every Trader

Our company prioritizes effective communication with clients, providing a professional support service to address all financial inquiries related to trading. Our team of experts is always available to assist with any questions and ensure seamless trading experiences.

News

Stay Up to Date With the Trends and Happenings

29.07.2026

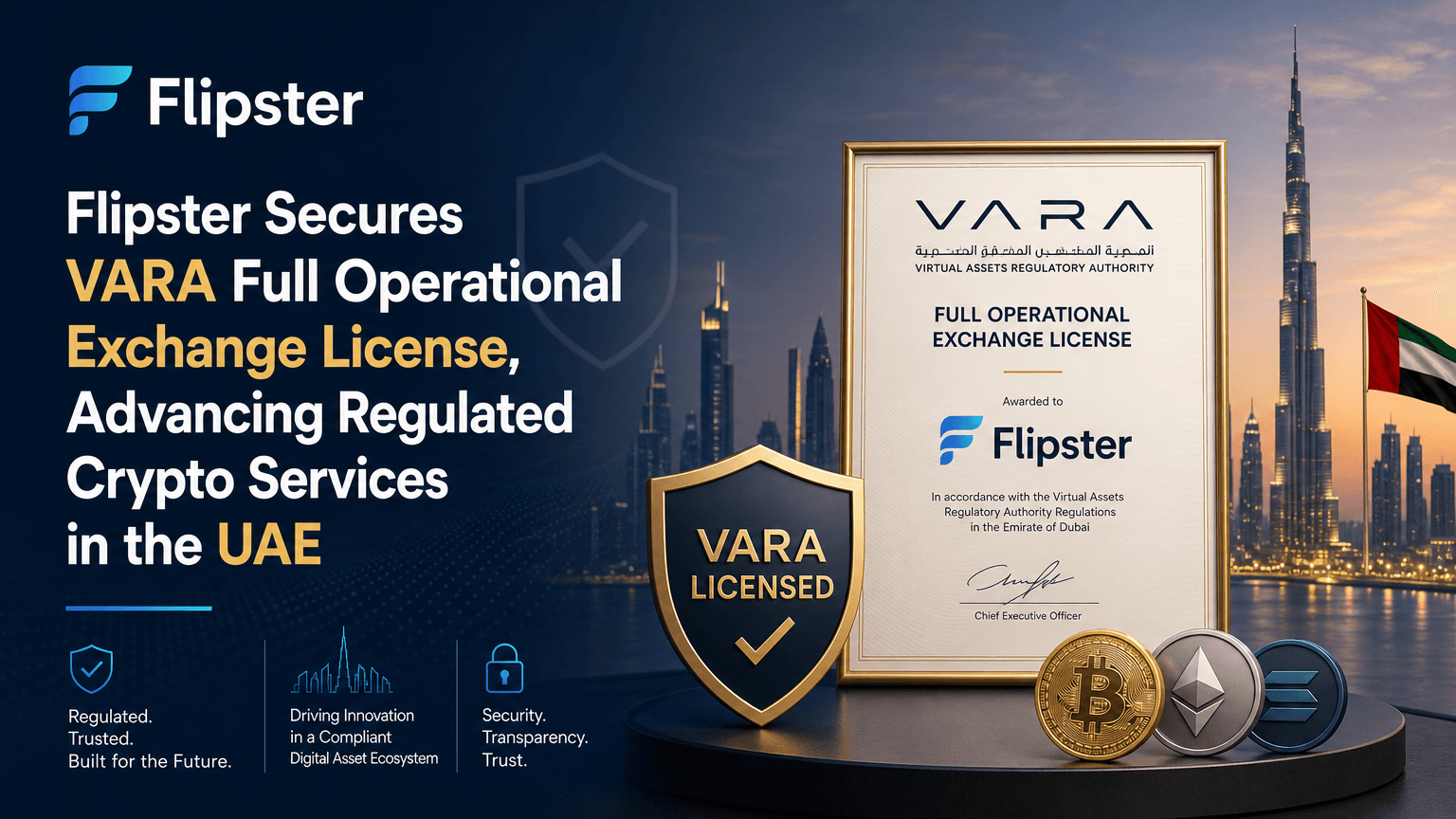

Flipster Secures VARA Full Operational Exchange License, Advancing Regulated Crypto Services in the UAE

Introduction to Flipster's Milestone Achievement

Flipster, a globally recognized cryptocurrency trading platform, has recently achieved a significant milestone by obtaining a full operational Exchange license (License No. VL/26/07/002) from Dubai's Virtual Assets Regulatory Authority (VARA). This pivotal authorization takes place under the entity Flipster FZE and marks the beginning of Flipster's regulated virtual asset services in the UAE, forming a cornerstone of their strategic global expansion plans.

Implications of the VARA License

The acquisition of this esteemed license empowers Flipster FZE to commence onboarding clients in the United Arab Emirates. This legal approval is not just a gateway to local market entry but serves as a launching pad for potential enlargement into a broader global user demographic. Providing users with trading exposure to both digital and traditional asset classes, Flipster's initial offerings will concentrate on spot trading. This will serve as the foundation for Flipster's regulated product suite, attesting to the platform's diverse and robust trading capabilities.

Understanding VARA's Regulatory Framework

Flipster's successful transition from a status of regulatory readiness and in-principle approval to being fully operational under VARA's framework is a testament to its adherence to regulatory standards. VARA's framework is acknowledged as one of the most exhaustive and globally recognized regulatory setups for digital assets. Operating under this framework equips Flipster with the ability to provide a secure and transparent transacting environment, supported by rigorous standards for custody, governance, and compliance, further enhancing user safety and access to digital assets.

Commitment to Global Financial Standards

This development underscores Flipster's commitment to achieving the highest standards in global finance. The platform is staunch in its belief that regulation is vital to building long-term trust within the trading community. VARA sets a lofty benchmark for balancing the advancement of innovation with the assurance of investor protection. This accomplishment not only solidifies Flipster’s presence in the Middle East but also showcases its dedication to maintaining a high standard of financial governance.

Leadership and Market Entry in the Middle East

Flipster's journey into the Middle Eastern market was initiated in May 2025 with the strategic appointment of Benjamin Grolimund as General Manager of Flipster FZE. The securing of the full operational license symbolizes the progression from merely entering the market to providing full-fledged, regulated services within one of the world's most progressive digital asset ecosystems. This move is not just a geographic expansion but an enhancement of the platform's service offerings to its users.

About Flipster

Founded in 2023, Flipster has swiftly positioned itself as a leading name in cryptocurrency trading. Built by traders for traders, Flipster offers deep liquidity, industry-leading leverage, and comprehensive coverage across global markets, catering to various trading styles and enabling traders to capitalize on market opportunities globally. The platform's unique proposition includes offering access to real-world asset perpetuals in supported jurisdictions, allowing users to trade both digital and traditional assets from a single, well-integrated platform. Additional details can be accessed via their official site flipster.io or by following their updates on X.

27.07.2026

LTO's Price Collapse of 44.34% Signals Market Turbulence

The Sudden Plummet in LTO Network's Price

In a thrilling and unsettling manner, the cryptocurrency market observed a startling event as LTO Network's price experienced a severe plummet, shedding a staggering 44.34% in mere 30 minutes. The asset's value nosedived from $0.0038 to a recently observed $0.002115, an occurrence that has sharply grabbed the attention of traders and financial analysts, underlining the elevated volatility present within the market. At a point where the 24-hour trading volume reached $155,144, the sudden and extreme price movement led to a wave of scrutiny and analysis as investors started to reassess their positions, contemplating the potential impacts and adjustments required in their trading strategies.

The Key Development

The key observation here is the extreme volatility demonstrated by LTO Network's price action. The marked drop over a concise period of time denotes not just a contraction in its value, indicated by a current market cap standing at $615,529, but also underscores the inherent unpredictability that characterizes cryptocurrency trading. The sharp decline followed a 24-hour increase of 18.6%, which serves to accentuate the stark contrast and volatility associated with the asset's price movement. This isn’t an isolated incident; rather, the broader crypto market is reflecting mixed signals, hinting that this abrupt price movement may be rooted in larger market dynamics and sentiments.

At a Glance

LTO's pronounced price volatility brings to the forefront questions revolving around current market sentiment and future stability. Present trading levels signal a pivotal moment for traders and investors, pushing them to remain vigilant as potential support and resistance levels are expected to emerge as the situation evolves further. This period represents a critical juncture for market participants, emphasizing the need for strategic patience and observation.

By the Numbers

The data delineates that LTO's price underwent a significant plunge within 30 minutes, from its zenith of $0.0038 to its nadir of $0.002115. This dramatic change encapsulates the volatility intrinsic to the crypto market, where even minute fluctuations can precipitate substantial price shifts. The 24-hour price range between $0.00211492 to $0.0038 further stresses the precarious state of play for LTO holders and traders, necessitating a diligent monitoring of market dynamics.

What Could Be Behind This Move

One might ponder the underlying reasons for such a drastic price drop. This decline may be interpreted in the context of the broader market, which is awash with mixed signals and swinging investor sentiment. It’s not uncommon for sudden sell-offs to transpire without an apparent catalyst, reflecting the deep-rooted risks associated with cryptocurrency trading. At this juncture, traders are strongly advised to maintain a keen eye on market trends and external influences that continue to shape price movements.

Key Levels to Watch

In light of these market dynamics, traders are intently observing LTO's price movements for any signs indicating stabilization or further decline. A critical support level is observed near $0.0021, while resistance is estimated around $0.0030. Breaching these levels could either signal persisting bearish sentiment or, conversely, a resurgence in investor confidence if prices rebound above the resistance level. The unfolding developments necessitate a strategic approach to trading, underscoring the importance of comprehending, adapting, and responding to these swift changes in market conditions.

24.07.2026

Arthur Hayes Acquires 1,332.5 ETH, Sparking Community Interest

The Buzz Around Arthur Hayes' Ethereum Acquisition

The Ethereum community is currently witnessing a surge in excitement following a significant transaction made by Arthur Hayes, co-founder of BitMEX. Hayes recently purchased 1,332.5 ETH, equivalent to $2.53 million. The acquisition has been confirmed by Lookonchain, a notable entity in blockchain analytics, indicating a reinforcing interest in Ethereum as a viable investment choice. As discussions proliferate across social media platforms regarding this particular transaction, the community is intently monitoring its potential impact on broader market trends, hinting at the apprehension that accompanies movements in digital currencies.

Why This Purchase Captivates the Community

The news of Hayes' recent Ethereum purchase has led to a notable increase in social media activity. Lookonchain had reported 23 likes and 2 retweets on their tweet concerning the transaction, indicating a significant level of engagement despite seemingly modest figures. This kind of attention illustrates how high-profile transactions can evoke curiosity and speculation in the Ethereum community and the cryptocurrency world at large. Within the backdrop of a crypto market showing mixed signals, Hayes' formidable buy reiterates the support influential figures still provide Ethereum, regardless of prevailing industry sentiments. Analysts and observers might interpret such a move as a bullish signal, projecting confidence in Ethereum's potential to offer long-term value.

Arthur Hayes' Role in Cryptocurrency

Arthur Hayes is no stranger to the limelight in cryptocurrency trading and investment sectors. His strategic purchase of ETH aligns seamlessly with a broader trend of growing interest among institutional investors venturing into the digital asset domain. The Ethereum community has been engaged in lively discussions pertaining to network upgrades and strategies concerning market positioning, both of which contribute to the amplified focus on this significant acquisition. Hayes' purchase underscores an ongoing belief in Ethereum's evolving ecosystem and its potential for substantial returns.

Market Implications and Trader Reactions

Traders and market analysts are vigilantly observing potential subsequent actions from Hayes or other market figures known for their substantial influence. Given the shifting dynamics of cryptocurrency markets, such high-profile purchases can often imply that savvy investors are laying groundwork in anticipation of future market shifts. The prevailing positive sentiment on social media platforms might prompt traders to seek additional signs of institutional interest in Ethereum. This kind of activity could foster increased price stability and potential upward momentum for Ethereum, offering some respite amidst the inherent volatility of the crypto space.

Conclusion: A Reflection on Confidence in Ethereum

The excitement surrounding Arthur Hayes' Ethereum purchase is a fascinating indicator of the cryptocurrency market's current state and its potential future direction. This transaction reflects significant confidence not only in Ethereum but also in the broader acceptance of digital assets by influential figures and institutions. As the community continues to dissect the implications of this move, it becomes increasingly clear that Ethereum, with its robust network and growing interest, remains a central figure in the digital asset conversation.

22.07.2026

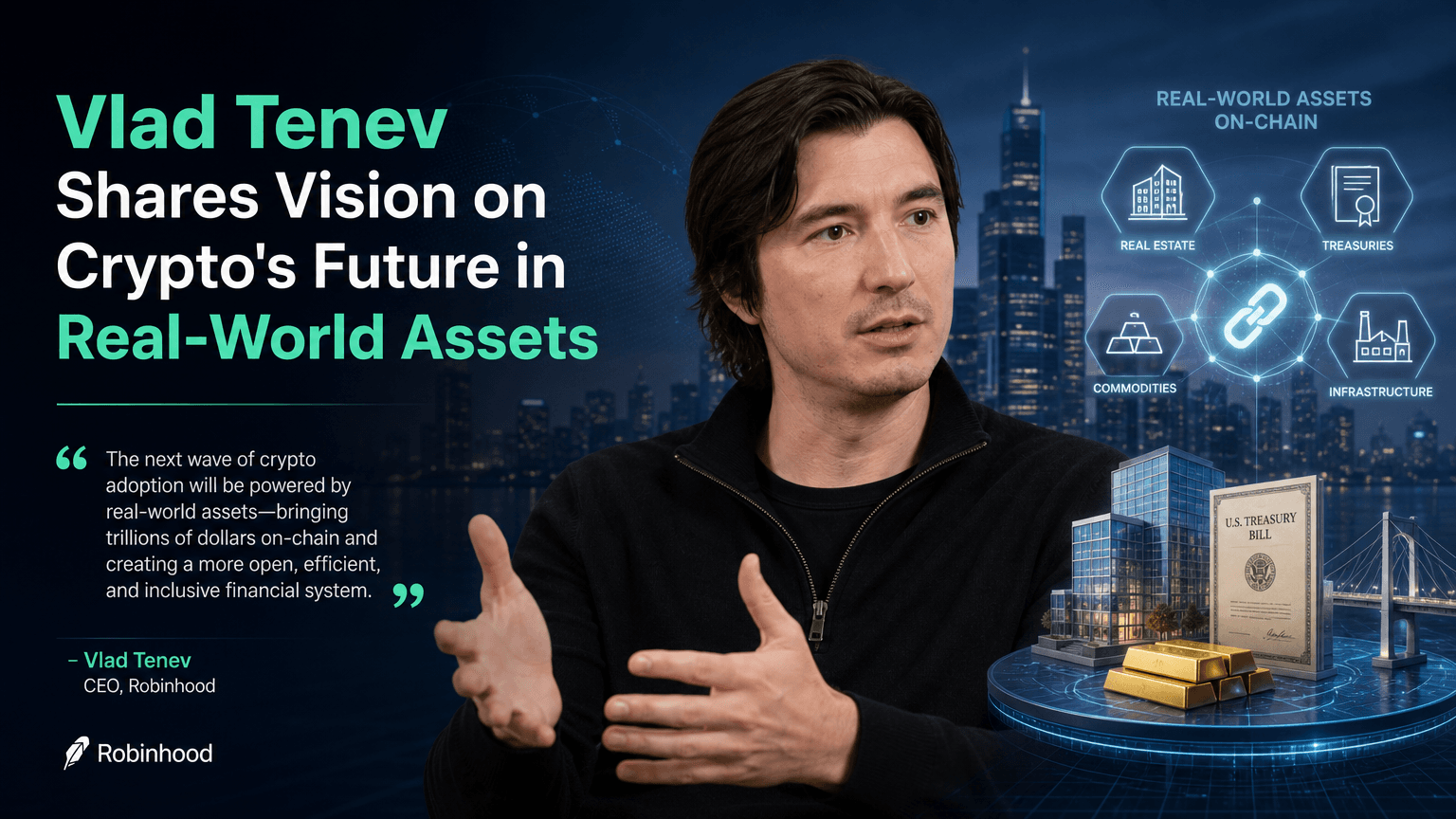

Vlad Tenev Shares Vision on Crypto's Future in Real-World Assets

Shifting Perspectives in the Crypto Space: The Role of Real-World Assets

The cryptocurrency market is a dynamic and ever-evolving landscape, often characterized by its rapid developments and the diverse range of opinions from influential figures within the industry. Recently, Vlad Tenev, co-founder of the popular trading platform Robinhood, has brought renewed focus to a vital topic with significant implications for the future of cryptocurrencies: the integration of real-world assets.

Vlad Tenev's Vision for the Future of Cryptocurrency

On July 8, 2026, Vlad Tenev shared his perspective in a tweet that has since ignited a robust discussion across the crypto community. His statement that "the future of cryptocurrency lies in real-world assets" underscores a critical shift toward practical applications and stronger ties between digital currencies and tangible values. Given the track record of Robinhood as a democratized trading platform that has enabled countless individuals to engage with financial markets, Tenev's insights carry considerable weight and influence.

Current Trends and Market Sentiment

The crypto market is currently experiencing a phase of mixed signals, with individual assets displaying varied momentum and price movements. This volatility is not unusual for cryptocurrencies, known for their fluid market dynamics and numerous external influences. However, Tenev's emphasis on real-world asset integration resonates at a moment when investors are increasingly seeking more stability and security in their digital holdings.

The Growing Relevance of Real-World Assets in Cryptocurrency

The concept of merging cryptocurrencies with real-world assets is gaining momentum, signaling a broader trend toward enhancing the utility and adoption of digital currencies. This approach can potentially offer a more stable and robust foundation for using cryptocurrencies as both investment vehicles and everyday transactional methods. Real-world assets can include anything from precious metals and real estate to everyday commodities, providing a tangible backing or linkage that can appeal to a broader audience of investors who may be cautious about entering the more speculative realms of crypto.

Potential Implications for the Future

As these discussions gain traction, traders, analysts, and regulators alike will be closely observing the developments in this area. The emphasis on real-world assets could drive significant changes in regulatory frameworks, prompting a reevaluation of how cryptocurrencies are integrated into mainstream finance. By providing a more concrete basis for value, cryptocurrencies could see increased legitimacy and acceptance in both corporate and consumer spaces.

Conclusion

The potential shift towards incorporating real-world assets into the cryptocurrency ecosystem marks an exciting frontier for the digital finance space. As the industry continues to mature, the inclusion of tangible assets offers a promising avenue for innovation, growth, and broader adoption of cryptocurrencies. Vlad Tenev's statement and the ensuing conversation among the crypto community are indicative of a transformative period that could redefine digital currencies’ role within the global financial system. As always, keeping an attentive eye on these developments will be crucial for investors and industry participants aiming to stay ahead in the ever-changing world of cryptocurrencies.

Want to Be a Part of a New Trading World?

Simply provide us with your email, and our manager will contact you to get started.